VACANCIES AVAILABLE

November 23, 2022

2023 BRANCH MEETING DATES

January 11, 2023

As seasoned Debt Counsellors, we know what this means. If you have not yet been practicing for long enough to know about these inner workings- I am here to give you a few clues as to why this article is titled as such.

December is not a fun season for Debt Counsellors, let us start there. It kicks off with the overwhelming black Friday deals (welcome new regret in January when the reality sinks in) gearing up towards silly season. Designed to entice consumers to spend beyond their budgets and taking on more credit than what is reasonably necessary to sustain the cost of living. The year ending, means that all who have worked so hard should be entitled to some reward or relief, right?

Consumers already under debt review

Debt review consumers already in the process are feeling left out of the fun and excitement, as they have hopefully been informed to start saving for annual costs as they entered the process. Life will throw curveballs at them, and at you. My advice is to use your critical thinking abilities and plan for any possible scenario that you will encounter. This includes court closures leading to termination notices requiring attention, as pay dates changed and systems get confused.

For a few lucky consumers, that dazzling December bonus will help them take advantage of the legitimate settlement offers that creditors have put on the table. (Plan ahead for dealing with that influx of queries from an admin perspective, or your December will not be relaxing at all!)

Expect the unexpected

You will face many interesting thought processes and plans consumers make for a tiny bit of respite from the traumatic bruising this year has left them with. Every year this is the theme, however, in 2022 it seems the battles have just been escalating. The credit industry itself has grown into a monster of sorts that cannot be contained.

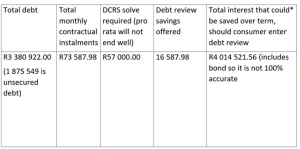

We, privileged few, see it every day in the assessments we conduct. The totality of the debt overwhelms the possibility to solve it. It falls outside the scope of what we can do. The tools we have (DCRS) are simply not able to cope with the sheer volume of debt that is in dire need of solving. As an example, I will use one assessment conducted where DCRS is in the exact window of opportunity to benefit consumer and creditor alike. Let’s put it in a nice table formula so that we can see the whole picture. We do after all speak more in numbers than words.

*Assessment projection based on information available at drawing credit report

Now for the twist. The consumer declines entering debt review because he needs the virtual rewards and cash back perks from these facilities. As Debt Counsellors, we can only attempt to convey what we know in hope they make decisions that are setting them up for financial success. We cannot let our personal needs to “keep the business running” overpower the consumer’s needs. Yes, that restructure fee would be nice to have. But I’m not going to “drop my quoted amount to sweeten the deal?” I know what will work and what will not. The sad truth is that a consumer in this mindset is not ready to undertake the process of debt review without the commitment required on their part. The choice is theirs.

If you have been in the industry long enough, you will know this will most likely end up with these possible scenarios.

1: They might get a “better deal” elsewhere at another debt counsellor. Who will need to increase the amount later as their assessment was not factoring in all variables. (This will eventually lead the consumer to join the gaping chasm of the abyss known as debt review limbo and perhaps even a nice NCR complaint against you, for failing their expectations in one way or another.)

2: This particular consumer could likely choose to get an additional loan (or five). Which would put them far beyond the point of assistance. One more loan mentality will end in a disastrous December, and a not-so-joyful-January. The power of denial can be very alluring.

3: They could end up considering sequestration instead. (I’m no expert, but I don’t think that is healthy for the credit industry and economy either. Not if the tipping point is breached.)

Planning for December

If Debt Counselling is your only form of income, I sincerely hope you planned in advance for yourself and your staff as well. The margin of error on projected income you could collect versus actual collection will need to be adjusted well in advance of the season. Be aware that the season does not end as the year does. Desperate December starts in mid-October and lasts until mid-February. As tempting as it might be to close your own business doors and take that break you also very desperately need, remember that your consumers need you now, more than any other time of the year.

The point of this article is to put yourself in every consumer’s mindset that you deal with- and actively look into the future of sustainability for them and for your business. Look ahead for their sake, your sake, and the economy’s sake.

Luckily, it isn’t all doom and gloom! There’s also a lot of excitement as we issue clearances and achieve many goals once perceived unattainable. After the last three years of stress and trauma, we have many things to look forward to in 2023. The industry is evolving, and as scary as that might be, we can all feel it heading in the right direction.

We only fear the unknown, so now that you have this information you can absorb it and devise a strategy to carry you through Desperate December ‘22. Perhaps there will even be some quiet time for reflection and planning to get you out of survival mode and into action- towards prosperity. As Ernest Hemingway said: “Courage is grace under pressure”

Time to tackle December head-on and conquer this year!

Written by – Nadia de Weerdt

SANDTON DEBT COUNSELLING – www.sandtondc.co.za

https://www.sandtondc.co.za/debt-counsellor/dcasa/

{kind=link}

{kind=link}